Lecture: 04

CONCEPT OF DEMAND & SUPPLY

Definition of Demand:

It is the quantity of

the good purchased at a given price in a given time.

Explanation:

The

word ‘demand’ is a desire of a buyer to buy. It is a relationship showing

various amounts of a commodity that a buyer would be willing and able to

purchase at alternative prices during a given time period, all other things

remains the same. Thus the definition of demand includes three components;

(a) Price of the commodity

(b) Quantity of the commodity

(c) Time

Note: that time period may vary. This can be week,

month, year etc.

For example:

Muhammad Ali purchased 1 kg of rice at

Rs.25 per kg last week.

This is the demand for rice

by Muhammad Ali.

Law of Demand:

The law of demand is given as, “If price of a commodity falls, its

quantity demanded increases and if price of the commodity rises, its quantity

demanded falls, other things remaining constant.” OR Demand is inversely proportional to Price and Quantity.

Demand Curve:

A

Demand Curve is a graphical representation of the relationship between price

and quantity demanded. It is a line or curve, in which point P is Price and Qd is quantity demanded. That point shows the amount of the good

buyers would choose to buy at that price.

Rise and Fall of Demand (or

Shift in Demand Curve)

When demand for a commodity goes up or down, not due to

price but due to other factors, the change is called rise (or increase) in

demand and fall (or decrease) in demand.

Example:

In Summer, the original demand (sale) of apples remains at 40 kilos

per day with the price of Rs.48 per kilo which increases in Winter

i.e. people buy 100 kilos per day which far ahead of 40 kilos per day

but price remains same. This is called increase in demand as depicted in table above.

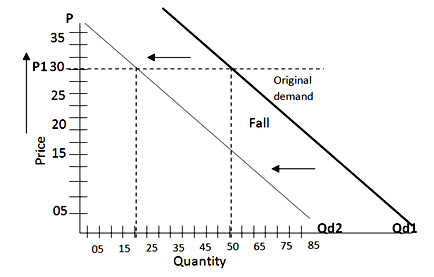

Fall in Demand:

When

the demand of commodity decreases not due to price but due to other factors the

change is called fall in demand.

1. Change in

Income.

2. Change in

Population.

3. Change in

Consumer Preferences (Tastes or Liking and Disliking).

4. Prices and

availability of related goods (substitutes and complements).

5. Advertisements

and Publicity.

6. Change in

income distribution.

7. Expectations

of future prices can affect current purchases.

8. Change in

quantity of money.

9. Expenditure.

No comments:

Post a Comment